How to beat the cashflow crunch

We recently advised a wholesale and retail business that was experiencing large fluctuations in its sales, profits and cash flow.

The business supplies goods to energy and rural businesses and is required to carry large stock holdings and significant credit accounts. Heavy rains also caused damage to the business’s stock and premises and it was unable to supply refrigerated goods for a period of 2 months.

The owners, William and Laura, wanted advice on how to improve their profit, better manage their cash flow and prevent the loss of income from future unplanned events.

This case study highlights the importance of small business owners understanding the true costs of running their business and factors influencing their profit and cash flow. It also provides guidance on how to structure funding arrangements for unique business circumstances and how to use insurance as a means of protecting business income.

Client issues

• Unsure of break-even sales level

• Not understanding the benefits of ratio analysis and budgeting

• Not enough working capital

• Inadequate business insurance

How the issues were resolved

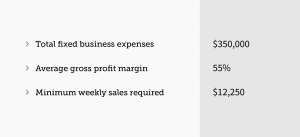

1. Breakeven Sales

William and Laura, with support from their accountant, completed a breakeven sales analysis enabling them to pin point the minimum sales required to cover their business expenses.

2. Improving Profit

To better manage their stock, William and Laura, with support from their accountant, completed a series of key profit ratio calculations. This included Gross Margin Return on Inventory and Gross Profit Margin. It was agreed William and Laura would upgrade their stock management system to improve their gross profit margin and to reduce shrinkage.

3. Improving Cash Flow

To improve their cash flow, William and Laura, with support from their accountant, completed a series of key cash flow ratio calculations. This included Account Receivable and Stock Turnover and a Flow of Funds Statement. It was agreed William and Laura would prepare a cash flow budget every year to determine their funding requirements.

4. Improving Cash Flow

William and Laura’s Financial Adviser was able to negotiate an extension on their overdraft limit to meet their working capital requirements. William and Laura’s Financial Adviser also purchased new Business Disruption Insurance to protect their business from a loss of future income.

Client Process

William and Laura completed a Business Life Plan to determine their business growth and succession objectives.

Stephen Noble – Director